Allocating to a trend-following strategy in high yield credit can improve both portfolio risk and return compared with traditional buy-and-hold strategies. This finding provides advisors with a valuable tool for managing client pressures, many of whom seek to increase stock market risk during boom times without sufficiently considering the risks their portfolios face during a downturn.

We recently discussed the risks facing investors who use time-honored, set-and-forget 60-40 indexing strategies. Now, we look at what can happen to a portfolio that supplements buy-and-hold by investing a meaningful proportion of assets in a trend-following strategy (also known as tactical asset allocation, or time series momentum) in high yield.

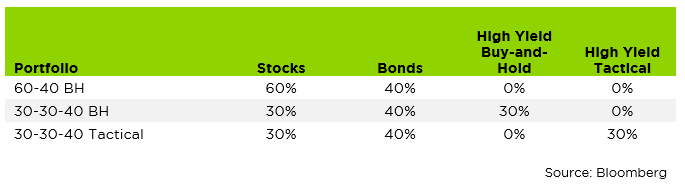

It turns out allocating away from an equity index and toward a tactical high yield strategy can modestly improve returns while potentially reducing portfolio risk. We evaluated historical returns for three types of portfolios: a traditional 60%-40% allocation between stocks and U.S. Treasuries; a passive buy-and-hold allocation to 30% stocks, 30% buy-and-hold US high yield corporate debt, and 40% U.S. Treasuries; and a portfolio with a passive buy-and-hold allocation to 30% stocks and 40% U.S. Treasuries, with the remaining 30% of assets invested in a tactical high yield.

As a reminder, note that high yield bonds entail greater risk of loss of principal when compared to higher rated forms of fixed income. In this case, however, high yield bonds’ impact on portfolio risk comes from our proposition to replace equity.

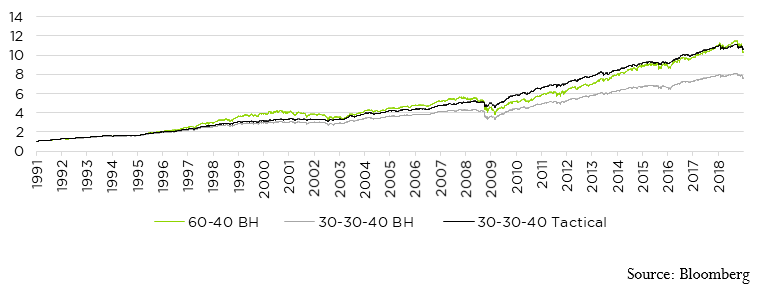

The historical results for each portfolio are shown below, from a return perspective:

Return: Impact of Replacing 50% of Equity Allocation with Tactical High Yield (1991-2018)

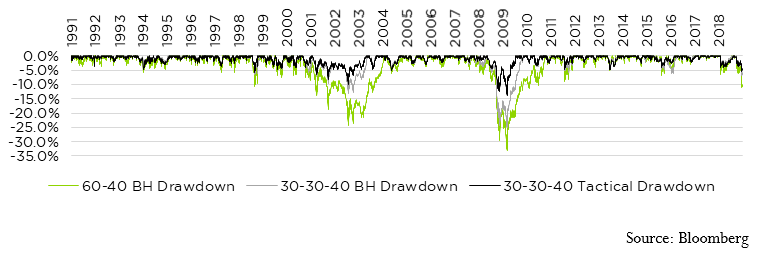

The same data set from a downside risk perspective:

Drawdown: Impact of Replacing 50% of Equity Allocation with Tactical High Yield (1991-2018)

(Note on time series construction: The bond asset class is represented by the Bloomberg U.S. Treasury 3-5 Year Total Return Index; stocks are represented by the S&P 500 Index; High Yield is represented by the Morningstar High Yield Category; The Tactical High Yield strategy is represented by being invested in the Morningstar High Yield Category when that index is above its 200 day moving average the prior day, or invested in the Bloomberg U.S. Treasury 3-5 Year Total Return Index when the high yield index closes below its 200 day moving average the prior day. This is a stylized example made with discretion, where intermediate duration treasuries are chosen instead of Bloomberg Barclays US Aggregate as the longer duration treasury index has a larger negative correlation to stocks, enhancing portfolio performance in times of market stress. None of these indexes include management fees or transaction costs, so real world performance would have certainly been lower in magnitude net of fees.)

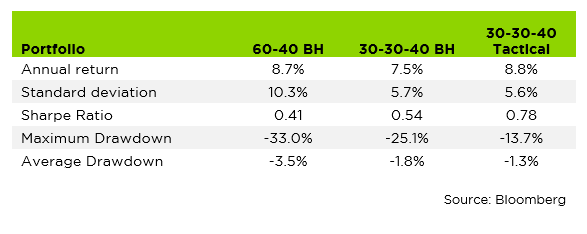

The first and most obvious conclusion is that a passive allocation to high yield meaningfully dampens returns. Investors who shifted half of their risky assets out of stocks and into a high yield index would have meaningfully underperformed investors who held traditional 60-40 portfolios from 1990 through 2018. This is not entirely surprising. High yield credit investments have historically lagged stocks in annual returns. In exchange for the lower return profile, investors who allocate to high yield typically experience smaller drawdowns compared with those who invest in stocks.

The more surprising conclusion comes when we shift from a buy-and-hold to a tactical allocation in high yield credit. Although such a portfolio experienced periods of underperformance compared with the 60-40 buy-and-hold portfolio (notably during the dot-com and housing booms of the 1990s and 2000s), it has lately outperformed, and across the past three cycles has delivered not only a relatively lower risk profile as measured by standard deviation, but also slightly higher average returns.

We believe the main benefit of a tactical allocation to high yield credit as a partial equity replacement is the reduced severity of portfolio drawdowns. Tactical strategies are designed to go “risk-off” when a risky asset class enters a downtrend, only resuming a “risk-on” posture when market trends are more favorable. This helps manage clients’ behavioral responses to declining portfolio balances. Normally, we’d expect a more favorable risk profile to accompany reduced long-term returns. For the period we’ve studied here, the benefits of allocation to tactical high yield are even greater than expected: The returns of this combination of indexes have historically experienced slightly higher annual returns while also reducing portfolio drawdowns.

Before we celebrate, we should remind readers that there is no free lunch, even in this analysis. The very attractive risk-reward profile in the blended stock/bond/tactical high yield strategy only accrues to investors who are disciplined enough to consistently implement the strategy, even during periods when it underperforms traditional buy-and-hold investments in stocks and bonds. To deliver on this strategy’s risk-management benefits, advisors must educate clients about the need for prudence and adherence to long-term strategy, even during heady times such as the dot-com and housing booms. But for risk-averse clients (more specifically, “conditionally” risk-averse ones) – especially those who run the risk of making harmful decisions during portfolio drawdowns, the rewards to a blended allocation between stocks and tactical high yield strategies can be substantial.